| STOCK MARKET LIVE | BSE | NSE | ||||||

West Asia conflict triggers jitters in equities, but what lies ahead?

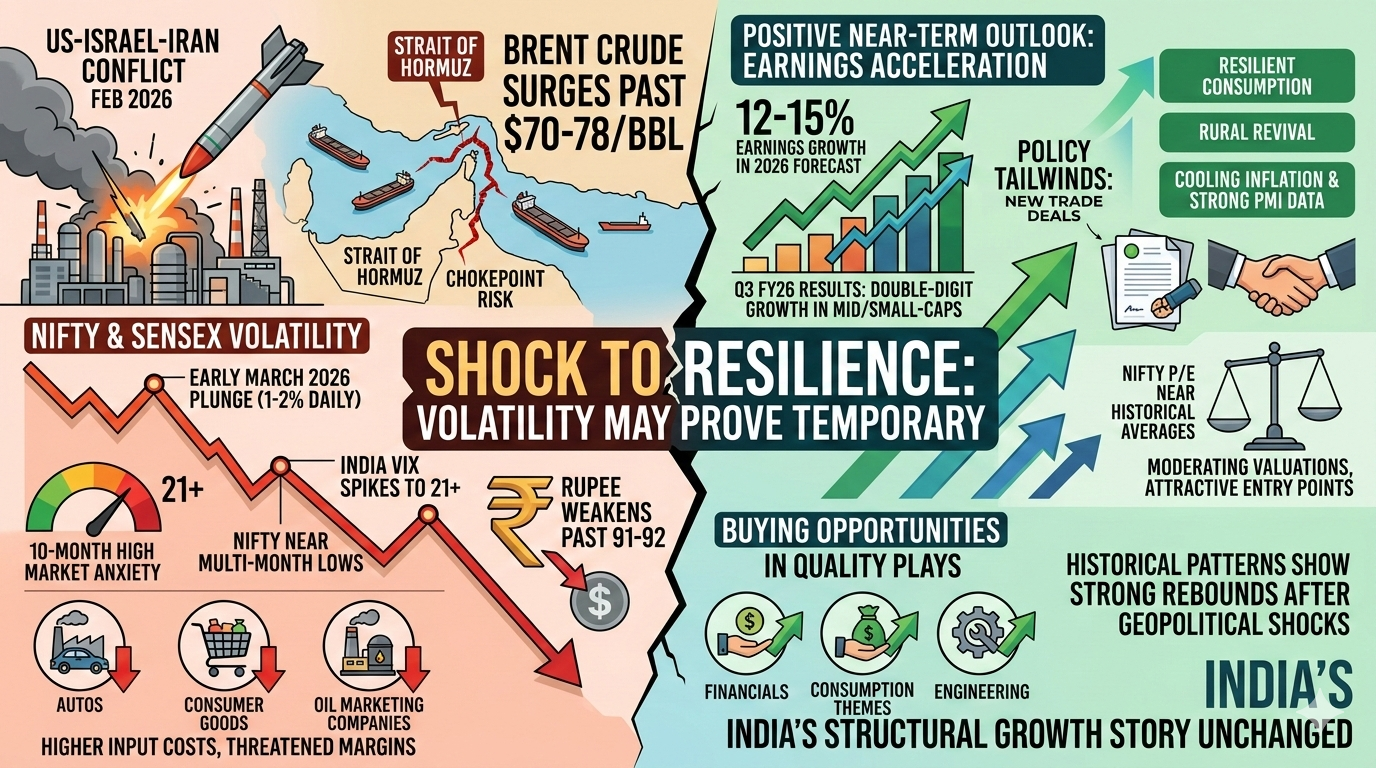

MUMBAI: Early March 2026 has been a trial by fire for Indian equity markets. As the Indian equity markets have been gripped by intense volatility due to the war in the Middle East, specifically the escalating US-Israel-Iran conflict, investors are navigating a turbulent phase marked by sharp sell-offs, surging crude oil prices, and heightened geopolitical uncertainty. Investors have watched with bated breath as the Sensex and Nifty grappled with intense volatility, driven largely by a storm of global headwinds. By March 5, the Nifty 50 had retreated 5.22% for the year to close at 24,765.90, while the Sensex saw a steeper decline of 6.11%, settling near the 80,016 mark.

The Indian equity markets have been gripped by intense volatility in early March 2026, with the Sensex and Nifty experiencing sharp declines amid global headwinds. As of March 5, the Nifty 50 had shed 5.22% year-to-date, closing at 24,765.90, while the Sensex fell 6.11% to 80,016. This downturn intensified on March 4, when the benchmarks tumbled over 1% in early trade, with the Nifty slipping below its 200-day moving average—a key long-term support level—marking a seven-month low. The India VIX, a gauge of market fear, surged 22% to 20.98 on March 4, its highest since May 2025, driven by escalating West Asia tensions and a 119% year-to-date volatility spike. Geopolitical jitters, including Middle East conflicts and surging oil prices, have triggered panic selling, with the Sensex crashing over 1,000 points on March 2 and pre-open indications of a 4,000-point drop earlier in the week.

As is known the roots of this instability lie in the protracted escalation of the West Asia conflict, which has evolved from localized skirmishes into a broader regional confrontation involving key energy-producing nations. This "perma-war" environment has fundamentally altered the risk premium for emerging market equities. Central to this anxiety is the weaponization of trade routes and the resulting surge in commodity prices.

The conflict, as naturally expected disrupted global energy supplies, particularly through threats to the Strait of Hormuz, a critical chokepoint for nearly 20% of world oil flows. Brent crude has surged significantly, climbing well above $70-78 per barrel in recent sessions, fueling inflation fears for oil-import-dependent economies like India. At the same time, Brent crude’s ascent toward the $100 mark has historically acted as a headwind for Indian stocks, raising fears of "imported inflation" and squeezed corporate margins.

Beyond energy, the conflict has ignited a rally in "safe-haven" commodities like gold, which often triggers a tactical rotation out of risk assets like equities. For India, a massive commodity importer, the spike in industrial metals and energy prices threatens the valuation multiples of high-consumption sectors. Equity investors are currently pricing in the potential for a prolonged period of high input costs, which could delay the anticipated recovery in operating margins. Consequently, the market has seen a sharp divergence: while commodity-linked stocks find temporary support, interest-rate-sensitive sectors like Financials and Auto remain under pressure as the prospect of RBI rate cuts is pushed further into the horizon.

These tremors reflect broader global uncertainties, including trade tensions and a weak start to the year for emerging markets. Foreign institutional investors (FIIs) sold heavily in 2025, exacerbating the outflow, while domestic resilience from DIIs provided some buffer. High valuations and muted earnings growth in 2025—estimated at just 3% for Nifty 50 companies—further dulled India's appeal, leading to underperformance against Asian peers.

Yet, amid the chaos, signs of stabilization are emerging, pointing to a positive near-term outlook anchored in robust earnings recovery. Brokerages like Goldman Sachs and J.P. Morgan forecast a mid-teen earnings growth of 12-15% for 2026, driven by consumption revival, lower input costs, and policy support. Q3 2025 results showed broad-based improvement, with mid-caps and small-caps posting 12% and 21% growth, respectively, fueled by festive demand and rural upticks in sectors like autos and consumer staples. Valuations have moderated significantly—the Nifty's price-to-earnings multiple dropped to 21.7 from 25.2, nearing historical averages making India more attractive to global investors.

Policy tailwinds bolster this optimism: Recent FTAs with the US, EU, and UK reduce trade uncertainties, boosting manufacturing, IT, and exports. Cooling inflation, stable growth, and improving PMI signal economic resilience. FIIs have turned net buyers in February, injecting $2.2 billion, as the rupee stabilizes and US markets appear overvalued. A market rebound on March 5, with the Sensex jumping 900 points, underscores this shift.

In essence, while short-term volatility from geopolitics persists, India's structural strengths earnings acceleration, fiscal prudence, and domestic demand—position equities for a 15-20% upside in 2026. Investors should focus on quality stocks in engineering, financials, and consumption themes, as the market transitions from caution to opportunity. The jitters may linger, but the fundamentals herald a brighter horizon.

Reporter

Rajesh is our Senior Consulting Editor, a veteran financial journalist and financial literacy educator. He brings a wealth of experience to his work, combining deep market insights and editorial integrity with top-tier journalism and publishing expertise.

View Reporter News